L4 Automatic Vehicle Market Growth Analysis Research Report By Vehicle Type: Passenger Cars, Commercial Vehicles, Robotaxis / Mobility-as-a-Service Vehicles, Autonomous Shuttles & Buses, Delivery & Logistics VehiclesBy Propulsion Type: Battery Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicles (PHEV), Hydrogen Fuel Cell Vehicles, By End User: Mobility Service Providers, Fleet Operators, Logistics Companies, Government & Smart City Projects, Private Consumers (Future Adoption) - and Global Forecast to 2034

Mar-2026 Formats | PDF | Category: Automotive | Delivery: 24 to 72 Hours

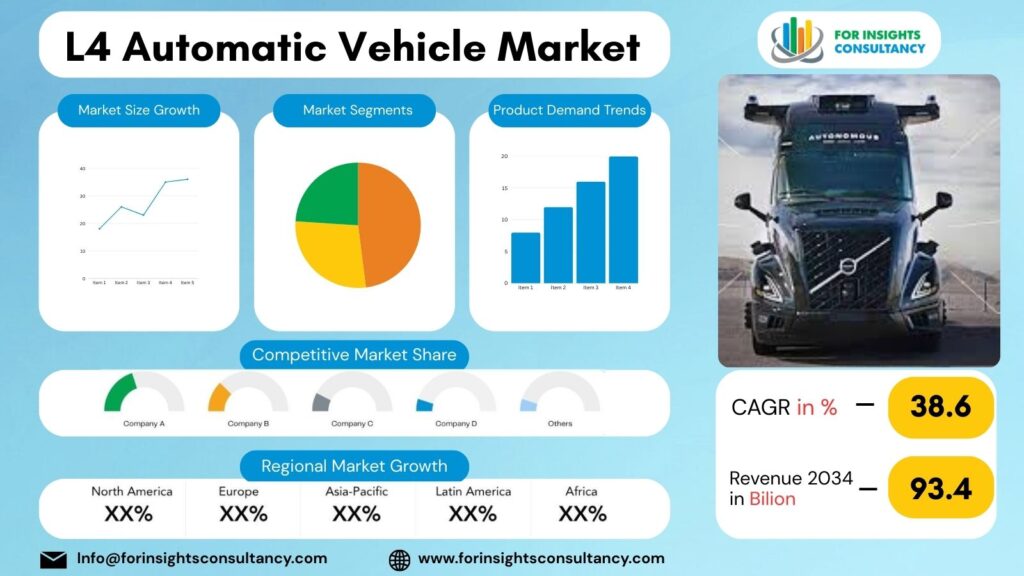

The Global L4 Automatic Vehicle Market is estimated to be valued at USD 23.8 Billion in 2025 and is predicted to reach USD 93.4 Billion by 2034, growing at a compound annual growth rate (CAGR) of 38.6% from 2026 to 2034.

L4 Automatic Vehicle Market: Overview and Growth in the Upcoming Year

The year 2026 is pivotal for the Level 4 (L4) autonomous vehicle market, as the industry is moving towards commercialization for the first time. For the first time, autonomous driving technology will be used outside of controlled pilot programs. Within designed operational design domains (ODDs), L4 Automatic Vehicle will be able to drive without the need for human engagement. This will make them an excellent fit for operational environments such as urban mobility corridors, logistics hubs, and smart city transport systems. Safer and more autonomous decision making made possible through the advances of artificial intelligence, sensor fusion, and high computing power are helping expedite industry confidence in autonomous vehicle large-scale deployments.

Increased investment from vehicle manufacturers, technology firms, and mobility service providers who are keen on transforming transportation efficiency and safety will be a key contributor to market expansion in the coming year. The introduction of more autonomous vehicle regulations in urban zones will encourage commercialization of L4s. Driver congestion issues in urban areas and the public transport systems will further support L4 Automatic Vehicle implementation.

Flexibility in real-time data analytics is allowing developers to modify and improve their systems in autonomous robotaxis and shuttle services expected to greatly grow in the coming years. Flexible and fleet-based deployment models are anticipated to allow developers greater control of their environments. Other emerging technologies geared towards logistics, such as autonomous last-mile delivery, and transport from warehouse to distribution, are expected to control more predictable and repetitious routes similar to those autonomous vehicles.

The combination of electric vehicles with autonomous systems (or driverless cars), as well as the aforementioned logistics, is expected to become normative. (It is probably, but not certain, to become the next integrating standard). The drive (pull) for these autonomous vehicles is primarily due to the reduction in operational costs and the requirement for more sustainable operational models, which is supported by growing legislative control for more sustainable policies in the majority of densely populated urban areas.

Significant improvements in both LiDAR (Light Detection and Ranging), Edge Computing, and V2X (Vehicle to Everything) systems provide breakthrough improvements in environmental perception. The aforementioned systems, coupled with improved operational safety, provide the ability for vehicles to better manage and contain overall traffic.

Growing advances in safety ensure the continued confidence in the use of autonomous vehicles. The cloud is enabling a quantum leap in the verification of autonomous driving (AD) algorithms and simulation in AD, allowing the validation of safety systems and service cycle improvements and predictive response.

Although many developers, including automakers, are remaining steadfast in their drive to develop autonomous systems, not one has focused on the dominant strategy (or defined best course of action) to ensure greater balance and seizure of developing markets and to provide adequate developer confidence.

The industry anticipates having an adequate level of public acceptance to support a greater number of autonomous vehicles being deployed in more diverse applications. The partnerships being developed among automakers, semiconductor manufactures, and software system developers is an additional indicator for eliminating strategy issues of risk/reward and/or developing autonomous systems that permit the scalable deployment of autonomous vehicles to meet the anticipated demand.

From the upcoming prospects, the L4 automated driving vehicle market will likely move away from the experimental phase towards early commercialization in 2026, especially in controlled urban and commercial mobility environments. L4 automation is positioned as the first building block toward fully autonomous mobility ecosystems for the upcoming decade due to further advancements in Artificial Intelligence (AI) systems, favorable governmental regulations and policies, and increased people’s need for cost-effective means of travel.

Market Dynamics 2026

Growth Drivers

Improvements in AI and Sensor Fusion

The real-world applicability of Level 4 autonomyy is becoming a reality due to the advancement of AI algorithms, multi-sensor data fusion (LiDAR, RADAR, and cameras), and machine learning models. This is due to the advancements in real-time situational and context awareness and decision making.

Safer Transportation Systems

Due to the desire to reduce or eliminate human errors in driving, Governments and transport companies are advocating for the development and implementation of fully autonomous driving technology and vehicles.

Mobility-as-a-Service (MaaS) and Robotaxi

With the continued development of driverless technology, shared autonomous service models will be able to support fleet-based autonomous transportation, leading to the rapid adoption of autonomous transport integrated with shared mobility services.

Driver Shortages in Logistics and Public Transport

The growing scarcity of commercial drivers is forcing autonomous solutions to be applied to logistics and transport systems to sustain operational continuity within the supply chain.

Restraints

High Expenses In Raw Construction And Deployment

When compared to standard automobiles, the production, construction, and deployment expenses of automobiles with Level 4 autonomous systems are much higher due to the advanced sensors, redundant safety systems, and high-level computing needed to be integrated into the new vehicles.

Expenses In Building And Deploying Vehicles With Level 4 Autonomous Systems

The absence of autonomous driving regulations globally leaves policymakers and systems developers with a multitude of unknowns due to the fact that regulations, directives, rules of accountability, and safety certifications are inconsistent from one region or country to the other.

The engineering requirements, limitations, and certifications associated with safety have been and will continue to be the greatest obstacles to the rationalization of autonomous system engineering and the resultant technologies.

Restricted Operational Design Domains (ODDs)

Vehicles with Level 4 autonomous systems are currently only capable of operating in a geographically limited area in a set of mapped urban environments or in a limited set of controlled route zones, and as a result, widespread and unrestricted use of these vehicles is extremely limited.

Opportunities

Expanding services to include Robotaxis and Autonomous Mobility

Fully automated taxi services are rapidly becoming one of the most profitable avenues for mobility as a service companies. By deploying driverless fleets, companies are able to reduce operational costs while increasing accessibility to automated transportation services in urban areas. Recent partnerships and funding within the industry suggest there is a clear and present demand for multi-city driverless transportation services within the next three years.

The growth of Autonomous Logistics and Last Mile Delivery

The logistics sector stands to benefit the most financially by incorporating autonomous vehicles to drive, optimize, and reduce route planning and workforce reliance for the first and final stretch of the urban delivery ecosystem. Productivity and supply chain efficiencies will continue to improve as autonomous vehicles are used to perform the same task repeatedly without a defined operational pause.

Software-Based Revenue Models (Autonomy-as-a-Service)

The emergence of Level 4 (L4) autonomous vehicles is to be expected given the performance of the industry to date. L4 represents the first true divergence in the development of autonomous vehicles as it moves the focus of value creation from the vehicle itself to the software ecosystem within the vehicle. This will allow for the first true software-as-a-service (SaaS) revenue models as companies will be able to license autonomous driving “intelligence” to be incorporated within various brands and fleets of vehicles.

Smart Cities and Integrated Connected Infrastructures

Autonomous vehicle services such as self-driving public transportation, autonomous service vehicles for mobility within a defined area, and self-driving shuttles will fill the urban mobility service paradigm as Level 4 (L4) vehicles are introduced. Cities that are equipped with smart traffic systems and connected flexible mobility infrastructures will create the ideal operational environment for deploying Level 4 autonomous vehicles.

Challenges

Safety Assessment in Real-World Scenarios

AI’s understanding of construction zones, mixed traffic, and unpredictable pedestrians, remains a challenge. Thus, L4 vehicles need to be able to safely navigate these unpredictable, real-world scenarios.

Reliance on Potentially Unreliable Systems

A standstill in vehicular movement and posed traffic dangers as a result of malfunctioning traffic signals and broken mapped systems demonstrate operational weaknesses of autonomous vehicles. These vehicles, as it is, find themselves immobilized by such scenarios as a broken traffic signal or broken mapped systems.

Threats to Safety and Privacy through Cyber Attacks

Because of a connected autonomous vehicle’s real-time data exchange with cloud systems, it is open to various threats such as hacking, data interception, GPS spoofing, and other unsafe and legitimate system attacks that may pose significant threats to its operating system.

Differing Regulations by Region

Mobility operators and vehicle manufacturers face challenges from the differing regulations on autonomous vehicle operation in differing locals. This results in a slowed down operational implementation and commercialization of the vehicle.

Top Companies Covered In This Report

L4 Automatic Vehicle Industry Company News

Waymo

News (2026): Announced plans to launch fully driverless ride-hailing services in London by late 2026, marking international expansion

Expanded robotaxi services into additional U.S. cities including Dallas, Houston, San Antonio, and Orlando, increasing operations to 10 major metropolitan markets.

Zoox

News (2026):

Accelerated testing of purpose-built robotaxi vehicles in U.S. cities as competition intensifies in autonomous ride-hailing markets.

AutoX

Continued expansion of fully driverless testing and urban robotaxi programs, focusing on dense city autonomous navigation development alongside Chinese autonomous driving initiatives.

Aurora Innovation

Advanced development of autonomous trucking platforms targeting commercial freight deployment, supported by collaborations with logistics and automotive partners.

Tesla

Increased focus on robotaxi strategy and autonomous driving software development amid growing competition from dedicated L4 mobility providers entering urban deployments.

Detailed Segmentation and Classification of the report (Market Size and Forecast – 2034, Y-o-Y growth rate, and CAGR):

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Robotaxis / Mobility-as-a-Service Vehicles

- Autonomous Shuttles & Buses

- Delivery & Logistics Vehicles

By Propulsion Type

- Battery Electric Vehicles (BEV)

- Hybrid Electric Vehicles (HEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hydrogen Fuel Cell Vehicles

By Component

- Sensors (LiDAR, Radar, Cameras, Ultrasonic Sensors)

- Control Units & Processors

- Artificial Intelligence Software

- Connectivity Modules

- Actuators & Drive-by-Wire Systems

By Automation System

- Perception Systems

- Localization & Mapping (HD Maps)

- Decision & Planning Software

- Vehicle Control Systems

- Safety & Redundancy Systems

By Application

- Ride-Hailing / Robotaxi Services

- Public Transportation

- Logistics & Last-Mile Delivery

- Industrial & Campus Mobility

- Personal Autonomous Mobility

By End User

- Mobility Service Providers

- Fleet Operators

- Logistics Companies

- Government & Smart City Projects

- Private Consumers (Future Adoption)

Regional Deep-dive Analysis:

The report provides in-depth qualitative and quantitative data on the L4 Automatic Vehicle Market for all of the regions and countries listed below:

North America

North America is expected to remain the most mature and commercially active region for Level-4 (L4) autonomous vehicle deployment in 2026, supported by a strong innovation ecosystem, favorable state-level regulations, and continuous real-world pilot expansion. The United States leads regional progress due to early adoption of autonomous testing frameworks and the presence of major technology developers and automotive OEM collaborations. Several U.S. states such as California, Arizona, Texas, and Florida have created regulatory sandboxes that allow driverless vehicle trials and commercial robotaxi services, accelerating commercialization timelines and enabling faster validation of autonomous systems under real traffic conditions.

In 2026, large-scale deployment momentum is increasingly driven by robotaxi and autonomous mobility-as-a-service models, rather than private vehicle ownership. Companies like Waymo are expanding driverless ride-hailing services across multiple U.S. cities, reflecting a shift from experimental pilots toward operational urban mobility networks. Continuous fleet expansion and growing weekly autonomous rides demonstrate improving consumer acceptance and operational reliability, positioning North America as the global benchmark for L4 commercialization maturity.

Europe

In 2026, Europe represents a structured but regulation-driven growth environment for Level-4 (L4) autonomous vehicles, characterized by strong policy governance, collaborative pilot programs, and gradual commercialization rather than rapid large-scale deployment. Unlike regions focused on early commercialization speed, European countries emphasize safety validation, legal harmonization, and public transport integration, creating a controlled pathway toward autonomous mobility adoption.

The European Union’s evolving regulatory framework, combined with national legislation, is enabling testing within defined operational domains while ensuring strict compliance with safety and liability standards required for driverless operation. Academic and regulatory analyses highlight that European deployment depends heavily on unified approval procedures and clearly defined safety assurance requirements for automated systems.

Germany continues to lead the European sub-region due to its early legal authorization for Level-4 autonomous driving in designated areas and strong automotive engineering ecosystem. Pilot projects involving autonomous shuttles, logistics vehicles, and robotaxi trials are expanding across urban environments, supported by collaborations between mobility platforms and automotive manufacturers. Planned robotaxi testing in Munich beginning in 2026 illustrates how Germany is transitioning from experimental validation toward supervised commercial mobility services.

The United Kingdom is emerging as a major innovation hub, supported by new automated-vehicle legislation and strong investment inflows into AI-driven autonomy developers. Large funding rounds for autonomous technology firms and planned robotaxi deployments in London demonstrate increasing confidence from global automakers and technology investors. These initiatives aim to integrate scalable autonomous software platforms into both shared mobility fleets and future consumer vehicles, signaling Europe’s shift toward software-centric autonomy models.

France and Spain are advancing L4 adoption primarily through public transport and smart-city pilot programs. Autonomous robobus and shuttle trials operating in controlled urban corridors are helping authorities evaluate safety performance, passenger acceptance, and operational efficiency in dense city environments. These deployments emphasize integration with existing transit systems rather than private ownership, reflecting Europe’s mobility-as-a-service orientation.

Asia-Pacific

In 2026, the Asia-Pacific region stands as the fastest-advancing ecosystem for Level-4 (L4) autonomous vehicles, driven by strong government participation, large-scale urban testing, and rapid integration of artificial intelligence into mobility systems. Unlike Western markets that prioritize gradual commercialization, Asia-Pacific countries emphasize real-world deployment, smart-city integration, and public transportation automation, making the region a global experimentation hub for driverless mobility. National industrial policies, digital infrastructure expansion, and dense urban environments collectively accelerate operational validation and consumer exposure to autonomous transport solutions.

China leads the Asia-Pacific L4 landscape through aggressive commercialization and regulatory evolution. By 2026, commercial driverless robotaxi services are operating across multiple major cities including Shanghai, Guangzhou, Shenzhen, Chongqing, and Hangzhou, where updated national rules allow fully autonomous passenger and cargo services without onboard safety drivers under defined conditions. These deployments represent one of the world’s first large-scale L4 commercial operations, providing massive real-world driving data and accelerating technology maturity. Government authorities are simultaneously introducing stricter safety regulations requiring autonomous systems to achieve performance comparable to attentive human drivers, signaling a transition from experimentation toward standardized commercialization.

Japan follows a distinctly different pathway focused on social-need-driven automation. With an aging population and driver shortages, Japan prioritizes autonomous shuttles and public-sector mobility rather than private ownership. Government-supported projects are deploying autonomous shuttle services in urban and administrative districts, using open-source autonomous platforms to establish standardized operational models for future nationwide adoption. Japan’s policy roadmap targets broader Level-4 deployment later in the decade, emphasizing reliability, safety certification, and municipal integration.

South Korea is emerging as an innovation-centric sub-market, supported by heavy investment in intelligent transport infrastructure and dedicated autonomous testing environments such as K-City. Level-4 autonomous buses and experimental vehicles are being validated in controlled smart-mobility zones, demonstrating full driverless capability without traditional driving controls. Government initiatives aim to commercialize autonomous taxi services and strengthen domestic AI mobility technology competitiveness within the region.

Middle East and Africa

In 2026, the Middle East and Africa (MEA) region is emerging as a strategic early-deployment market for Level-4 (L4) autonomous vehicles, characterized by government-led innovation programs, smart-city investments, and controlled urban mobility ecosystems. Unlike mature automotive markets where regulatory complexity slows deployment, several MEA countries are adopting top-down policy frameworks that enable faster testing, licensing, and commercialization of driverless transport solutions. The region’s focus is less on private autonomous ownership and more on robotaxis, autonomous shuttles, and smart public mobility integration, positioning MEA as a practical testing ground for scalable L4 operations.

The United Arab Emirates (UAE) leads regional adoption and has become one of the world’s first locations to transition from pilot testing to commercial driverless services. In 2025–2026, Abu Dhabi launched fully driverless Level-4 robotaxi operations under government supervision, marking the first commercial deployment of autonomous vehicles in the Middle East without onboard safety drivers. Authorities introduced real-time monitoring platforms and structured licensing frameworks to ensure operational safety and compliance, reflecting a strong regulatory readiness for autonomous mobility integration.

Beyond Abu Dhabi, the UAE continues expanding autonomous mobility ambitions through luxury robotaxi fleets and AI-driven transport programs planned for 2026, reinforcing its long-term strategy to become a global hub for intelligent transportation innovation.

Saudi Arabia represents the second major growth center within the Middle East, driven by national modernization initiatives and smart mobility investments aligned with Vision-based economic diversification programs. Autonomous robotaxi passenger services began operating on selected routes in Riyadh, supported by national transport regulators and partnerships with global autonomous technology companies. These deployments allow controlled real-world testing while familiarizing citizens with driverless mobility concepts, accelerating public acceptance and operational learning.

In contrast, Africa remains at an early adoption stage but shows growing long-term potential. Autonomous vehicle activity is primarily concentrated in research pilots, logistics experimentation, and smart-mobility feasibility programs within technologically advancing urban centers. Infrastructure variability, regulatory development needs, and investment constraints currently limit large-scale deployment; however, rising urbanization and mobile-first digital ecosystems create future opportunities for autonomous shuttle and delivery applications, particularly in high-density metropolitan areas.

Frequently Asked Questions with Answers

What is the L4 Automatic Vehicle market size and growth forecast?

L4 Automatic Vehicle Market is projected to reach a value of USD 13.4 Billion in 2025 and is anticipated to grow to approximately USD 93.4 billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 38.6% during the forecast period from 2026 to 2034.

Who are the key players in the L4 Automatic Vehicle market?

The L4 Automatic Vehicle Market Includes Major Companies Waymo, Cruise, Baidu Apollo, Pony.ai, AutoX, Aurora Innovation, Zoox, Nuro, Plus, Torc Robotics, Tesla, Stellantis, Others.

What are the current and future trends for L4 Automatic Vehicle market?

L4 Automatic Vehicle market is shifting from pilot testing to commercial robotaxi deployment, driven by AI-powered autonomy, high-performance computing, strategic partnerships, and expansion into shared mobility and logistics applications through 2030.

Which regions dominate the L4 Automatic Vehicle market?

North America and Asia-Pacific dominate the L4 Automatic Vehicle market, with Europe emerging as a strong regulatory-driven growth region.

Key insights provided by the report that could help you take critical strategic decisions?

- Regional reports analyse product/service consumption and market factors in each region.

- Reports highlight possibilities and dangers for suppliers in the L4 Automatic Vehicle Market business globally.

- The report identifies regions and sectors with the highest growth potential.

- It provides a competitive market ranking of major companies, as well as information on new product launches, partnerships, business expansions, and acquisitions.

- The report includes a comprehensive corporate profile with company overviews, insights, product benchmarks, and SWOT analysis for key market participants.

Customization: We can provide following things

1) On request more company profiles (competitors)

2) Data about particular country or region

3) We will incorporate the same with no additional cost (Post conducting feasibility).

Any Requirement Contact us: https://www.forinsightsconsultancy.com/contact-us/

Table of Contents

For TOC Contact us: https://forinsightsconsultancy.com/contact-us/