In Vitro Diagnostics Market Growth Analysis Research Report By Product/Service: Reagents & Kits, Instruments/Analyzers, Software & Services, By Technology: Immunoassays, Clinical Chemistry, Molecular Diagnostics, Hematology, Microbiology, Point of Care Testing (POCT), Others (Coagulation, Urinalysis), By Application: Infectious Diseases, Oncology, Cardiology, Diabetes, Nephrology, Gastroenterology, Autoimmune Diseases, Others - and Global Forecast to 2034

Mar-2026 Formats | PDF | Category: Pharma & Healthcare | Delivery: 24 to 72 Hours

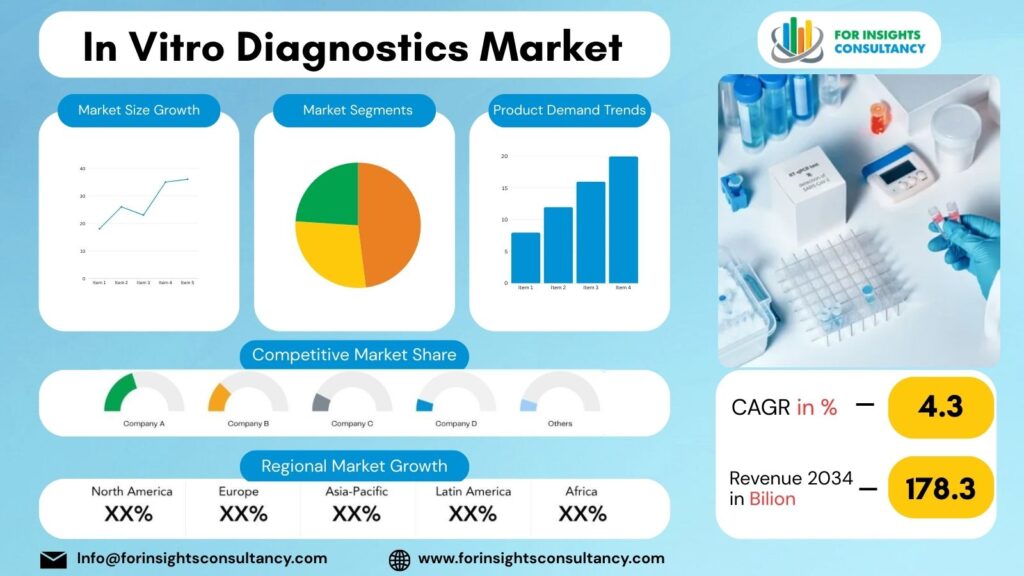

The Global In Vitro Diagnostics Market is expected to be valued at USD 113.9 Billion in 2025 and is anticipated to reach USD 178.3 Billion by 2034, growing at a compound annual growth rate (CAGR) of 4.3% from 2026 to 2034.

In Vitro Diagnostics Market: Overview and Growth in the Upcoming Year

The IVD (In Vitro Diagnostics) market offers crucial services to healthcare systems right from the detection of diseases, monitoring, and the management of treatment by providing lab services outside the patient’s body. It provides diagnostic solutions from various body fluid samples (i.e. blood, urine) and tissues so that health care providers can make informed clinically relevant decisions. Furthermore, In Vitro Diagnostics technologies are being utilized in hospitals, labs, and decentralized care settings due to the shift in healthcare services toward personalized and preventive services.

The market is expected to grow in 2026 and will likely continue to grow in the following years due to the changes in healthcare in a bigger span such as changes in policies instead of changes in the market. Due to the high prevalence of chronic diseases, early identification of and intervention in diseases, quick clinical decision-making, and prolonging the lifespan of individuals in developed and developing countries, there has been a rise in the number of tests needed to identify and manage chronic diseases such as cardiovascular and diabetes, cancer, and infectious disease.

Technology innovation has always fostered remarkable growth. Laboratory automation, artificial intelligence in diagnostic coding, and highly sensitive molecular tests are becoming more precise while their turnaround time is decreasing. Smaller, diagnostic, testing devices are paving the way for portable testing devices. This is letting testing assistants and communicators provide more testing to their patients. This is also allowing their patients to get testing and results nearer to them. This is very useful to regions with fewer testing labs.

The 2026 diagnostic ecosystems are expected to be more data supported than previously. Newer, diagnostic, testing, health and IV technology are expected to improve clinical diagnoses. Their integration is expected to improve diagnoses and is expected to be more efficient. This is very useful to regions with fewer testing labs.

Economic experiments are being conducted in the field. Newer, diagnostic, health, testing devices are expected to partner with the biotechnical and health provider in order to quickly complete the prototype and testing approvals.

By region, increased healthcare investments across the Asia-Pacific region, advanced healthcare technology in North America, and higher than average regulatory compliance in Europe will all contribute to demand across the regions in 2026. Developing countries are receiving higher investment in diagnostic labs and screening initiatives, broadening the overall market.

The market’s challenges are pricing pressures, lack of consistent reimbursement, and regulatory complexity, however, innovation, clinical education, and the focus of healthcare on prevention will provide sustained growth.

The In Vitro Diagnostics market in 2026 will be positioned in the forefront of the Integrated Healthcare System, moving away from traditional diagnostics to advanced, more efficient, and more patient centered diagnostics.

Market Dynamics 2026

Growth Drivers

Developing Interest in Preventive Disease Identifying

Due to the need to deal with issues relating to the costs and also the outcome of the patients) developing interest in disease preventive identifying is resulting in the hospitals and clinics increasing the order of diagnostic testing and ultimately their routine diagnostic testing.

Developing Interest in Chronic Disease Management

The growing range of chronic diseases which includes diabetes, disease of the heart and blood vessels, cancers and diseases of the kidney). This leads to developing interest to focus of the IVD (in-vitro diagnostics) solutions.

Extending Healthcare Innovations

As the focus of the government and the health care allow the focus on the treatment of disease to of the care of provide preventive screening of the diseases and also the diagnostic care of the patient.

Developing Interest in Molecular Diagnostics

As the focus of testing are the disease – the rapid developing of the testing and the of increasing interest is opening the market.

Developing Interest in Testing

As the testing is done closer to the patients, there are less dependence on the laboratory and the rest of the patients, the results are improving the access to the care of the patients.

Restraints

Expensive Technologies Used for Advanced Diagnostics

Small labs and financial strained healthcare sites find it hard to make use of complex diagnostic devices and the molecular testing systems as these require huge financial investments.

Long Processes for Getting Regulatory Approval

There are many steps needed for a diagnostic device to meet the different and multiple regulatory standards and clinical validation prior to it being released to the market. These steps tend to take a very long time which means that more advanced diagnostic methods take longer to be accessible and cover more healthcare needs.

Unpredictable Reimbursements and Pricing

There is a large focus on controlling and monitoring costs in healthcare. This directly affects the diagnostics providers because of the higher possibility of little to no reimbursement for the services performed.

Lack of Professionals in the Laboratory

The advanced diagnostic systems require the use of specialized trained staff and due to the existing gaps in the workforce in the various regions, it adversely affects the system’s initial and ongoing efficiency.

Opportunities

Expansion of Personalized and Precision Medicine

The medical field’s reliance on specific markers is growing. This opens a positive pathway for diagnostic companies to create specialized tests to support target therapies.

Growth of Decentralized and Point-of-Care Diagnostics

The growing trend of healthcare moving to patients, rather than patients going to healthcare, is creating opportunities for compact and rapid diagnostic systems.

Rising Adoption of Home-Based Testing Kits

The consumer demand for remote health monitoring and more convenient ways to manage chronic health conditions, test for infectious diseases, and monitor fertility is driving innovation and more self-testing options.

Integration of Artificial Intelligence in Diagnostics

For the first time, automated data interpretation has made diagnosing, analyzing, and result interpretation more accurate and has made it possible for clinicians to make decisions faster.

Challenges

Finding a Balance between New Technologies and the Law.

New tools and technologies used for the sidestreaming and diagnostics service are often created and handled before the patient and consumer registration and clinical evaluation tier and pricing feedback and consumer safety services are established.

Cost Effectiveness of Healthcare Systems.

Greater pricing and service consumer safety and consumer feedback evaluation and clinical assessment are now shown for the more costly diagnostic services.

Integration of a Range of Technologies.

Modern diagnostic services are an amalgamation of molecular diagnostics, immunodiagnostics, automation, and digital technologies.

The Modern Diagnostic Services are an Integrated System of…

A large number of advanced diagnostic technologies generate a volume of clinical data and data (results) that need trained professionals to analyze and find the most cost-effective results.

Top Companies Covered In This Report

- Abbott Laboratories

- Agilent

- Becton Dickinson

- bioMérieux

- Bio-Rad

- Danaher Corporation

- DiaSorin

- Exact Sciences

- Fujifilm

- Gold Standard Diagnostics

- Grifols

- Hologic

- Illumina

- LabCorp

- Qiagen

- Quest Diagnostics

- QuidelOrtho

- Roche

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

In Vitro Diagnostics Industry Company News

Abbott Laboratories

News (2026): Abbott announced a landmark agreement to acquire Exact Sciences for approximately $21–23 billion, marking one of its largest healthcare acquisitions in nearly a decade. The deal strengthens Abbott’s position in oncology diagnostics by adding advanced cancer screening solutions such as non-invasive colorectal cancer tests. The transaction is expected to close in 2026, expanding Abbott’s diagnostics revenue base significantly.

Agilent Technologies

News (2026):

FDA Approval for Companion Diagnostic (2026)

Agilent received regulatory approval for its PD-L1 IHC 22C3 pharmDx companion diagnostic, supporting immunotherapy treatment selection in ovarian cancer, strengthening its precision medicine portfolio.

Becton, Dickinson and Company (BD)

Strategic Diagnostics Business Restructuring (2025–2026):

BD announced a $17.5 billion merger of its Biosciences & Diagnostic Solutions division with Waters Corporation through a Reverse Morris Trust structure. The move aims to expand diagnostic capabilities and increase recurring revenue streams

Bio-Rad Laboratories

Ongoing Molecular Diagnostics Development (2026)

Bio-Rad remained active in genomics and molecular testing innovation, with industry reports highlighting continued investments in PCR and advanced diagnostic technologies to support clinical laboratories and research institutions.

Detailed Segmentation and Classification of the report (Market Size and Forecast – 2034, Y-o-Y growth rate, and CAGR):

Segment By Product Type

- Instruments (Analyzers & Diagnostic Systems)

- Reagents & Kits

- Software and Data Management Solutions

- Consumables and Accessories

Segment by Application

- Infectious Disease Testing

- Oncology (Cancer Diagnostics)

- Cardiology Testing

- Diabetes Monitoring

- Autoimmune Disease Testing

- Nephrology Testing

- Genetic & Prenatal Testing

- Drug Monitoring & Toxicology

- Neurological Disorder Diagnostics

Segment by Technology

- Clinical Chemistry Diagnostics

- Immunoassay / Immunochemistry Testing

- Molecular Diagnostics (PCR & Genetic Testing)

- Hematology Diagnostics

- Microbiology Testing

- Coagulation & Hemostasis Testing

- Next-Generation Sequencing (NGS) Diagnostics

- Point-of-Care Diagnostic Technologies

Segment by End User

- Hospitals and Clinical Laboratories

- Independent Diagnostic Laboratories

- Academic & Research Institutions

- Physician Offices & Clinics

- Home Healthcare Settings

- Blood Banks and Screening Centers

Segment by Testing Location

- Central Laboratory Testing

- Point-of-Care Testing (POCT)

- Near-Patient Testing

- Home-Based Testing

Segment bySample Type

- Blood Samples

- Urine Samples

- Tissue Samples

- Saliva Samples

- Other Body Fluids

Segment by Distribution Channel

- Direct Sales to Healthcare Providers

- Distributor & Channel Partner Networks

- Online Diagnostic Platforms

- Institutional Procurement Programs

Regional Deep-dive Analysis:

The report provides in-depth qualitative and quantitative data on the In Vitro Diagnostics Market for all of the regions and countries listed below:

North America

As the largest and most advanced regional market for In Vitro Diagnostics (IVD) North America is expected to maintain its number one position in 2026. This is due to the strong healthcare spending and the rapid adoption of advanced diagnostic technology for automation, precision medicine, and molecular testing.

IVD was estimated to generate $56.9 billion in 2026 for North America, due to the increase in the number of chronic illnesses, the increases in the number of people who participate in preventative healthcare, and the increase in illnesses that would require the screening of the patients to ascertain the need for the testing.

North America has the largest single market for IVD and has the largest market share of the IVD with approximately 40%. This is the result of their advanced diagnostic technology and strong regulatory frameworks that support the implementation of quality IVD.

Over the next five years, North America is expected to become the first region to use AI for clinical decision making and to use diagnostic technology that is both decentrally and digitally connected to the point of care.

- North America is the world leader in diagnostic technology for North America and holds the largest share of the North American IVD market.

- Large healthcare ecosystem with more than 280,000 medical laboratories with supportive diagnostic services

- Strong commitment to automated analyzers and cutting-edge molecular testing

- High penetration for diagnostic services in the areas of oncology, genetics, and infectious diseases

- Presence of leading global diagnostic players and R&D institutes

The country performs overwhelmingly high tens of billions of diagnostic tests every year, which signifies the country’s reliance on laboratory diagnostics for the management and clinical decision-making for testing and treatment of diseases.

Diagnostic services testing market in Canada

Canada is stable and innovation-oriented diagnostic market in North America.

Market Attributes

- Universal Health Coverage provides easier access to diagnostic services

- Growing number of molecular diagnostic labs

- Increasing uptake of telehealth testing

- Government funding in personalized medicine

- Canada’s contribution is justified with strong public healthcare systems and digital healthcare.

- Diagnostic services testing market in Canada

- Canada is stable and innovation-oriented diagnostic market in North America.

Market Attributes

- Universal Health Coverage provides easier access to diagnostic services

- Growing number of molecular diagnostic labs

- Increasing uptake of telehealth testing

- Government funding in personalized medicine

- Canada’s contribution is justified with strong public healthcare systems and digital healthcare.

Mexico

Mexico is an emerging growth sub-region with improved healthcare access and expanding diagnostic infrastructure.

Market Attributes

- Fast growth of private diagnostic laboratory chains

- Improved healthcare modernization

- High demand for diagnostic services at an affordable price.

- Growth is supported by government healthcare programs and increased awareness of disease screening, especially in urban centers.

Europe

In 2026, Europe remains an advanced, regulation-led market with strong public healthcare systems, laboratory infrastructure, and emphasis on preventative care, Europe’s public healthcare systems continue to grow. The region’s infrastructure has responsive, adaptable systems in place to accommodate the shift towards an emphasis on precision medicine. This fosters the integration of molecular diagnostics, automated systems, and digital laboratory solutions to further streamline and improve clinical decision-making.

Western Europe, specifically Germany, France, and the United Kingdom, continues to lead the region in market adoption and revenue contribution due to established reimbursement policies and a robust healthcare market. Germany has powerful clinical laboratory networks and modern labs. France has community based diagnostic programs and a focus on early disease detection due to fully covered programs. The United Kingdom has modern community based diagnostic programs leading to increased demand for modern, rapid testing. Hospital and central lab systems have invested in modern systems and instrumentation for increased testing volumes for cancer, communicable disease, and genetic testing.

Northern Europe is experiencing steady growth from the integration of digital healthcare and the use of data-driven connected diagnostic systems. In particular, Scandinavian countries (i.e., Sweden, Denmark, and Finland) are integrating diagnostic tools with electronic health records to provide real-time, actionable clinical insights and streamline the patient pathway. In addition, preventive screening programs, as well as the monitoring of population health, are initiatives that sustain the demand for testing in these countries.

Southern Europe is slowly emerging with growth from the development of healthcare technologies and the modernization of diagnostic services. Southern European countries, especially Italy and Spain, labor under health systems that are budget-driven including the expansion of lab automation and the creation of easy access to high-level testing options. Government programs designed to improve efficiency in hospitals and to reduce the time it takes to receive test results are driving demand for portable (or easily accessible) diagnostic tools.

Within the Eastern European region, new growth potential lies in countries like Poland, the Czech Republic, and Hungary, where diagnostic services are improved by combining private and public resources in lab infrastructure development and the new European health care funds. In addition to the quick access to health care, it is of great sign to be aware of new possibilities for early diagnosis. Routine test procedures in the healthcare systems are driving demand for diagnostic tools, as long as the prices are low and the controls are easily and quickly adaptable.

In 2026, updated diagnostic compliance frameworks’ regulatory harmonization across Europe encourages innovation and higher quality standards, driving Manufacturers to develop more sophisticated assays and clinically validated alternatives. With sustainability influencing purchasing decisions, healthcare systems are leaning towards procurement of energy-efficient instruments and solutions that minimize waste in laboratories. Europe’s IVD market growth, stems from an optimally balanced mix of tech innovation, accessible healthcare, and policies focused on expanding diagnostics. This provides the region with a stable and innovative market.

Asia-Pacific

The IVD market in the Asia Pacific is expected to continue growing in 2026 due to modernized healthcare systems, improved awareness about the importance of diagnosing illnesses, and the growing technologies used in clinical systems. The healthcare systems in the region are shifting focus from treating existing conditions to preventing and detecting illnesses, which will drive demand for testing and diagnostics. Government initiatives and infrastructure investments will drive an increase in testing in urban populations and those who develop illnesses due to poor lifestyles.

China accounts for the majority of healthcare remodel growth for the Asia Pacific region, which includes large scale biotechnology development. As patient volumes continue to grow, hospitals and diagnostics labs are implementing more automation systems. In addition, there is growing molecular diagnostics and infectious disease surveillance in secondary cities. There is innovative dependency on local diagnostic systems due to the collaboration between public hospitals and local manufacturers.Japan is a technologically sophisticated subregion with a strong diagnostic sense and high clinical efficacy standards.

The demand is due to the aging population. This demand is mainly due to the need for oncology testing and genetic testing. Chronic disease monitoring is also a Healthcare providers are using automated analyzers along with Lab integrated systems to improve efficiency and to decrease the time taken for test results. The culture of preventive screening and the regular health check Service programs have great influence on the steady demand for diagnostics throughout the health care system.

India has a faster emerging IVD developing market in the Asia Pacific by 2026 due to the developing private diagnostic chains, developing middle-class healthcare affordability, and the developing awareness on preventive testing. Diagnostic services have been expanded through the hub and spoke laboratory model to sub metropolitan regions. Affordable testing and point of care diagnostics have increased access to broad coverage and have significantly decreased the time to diagnosis within the resource deprived setting. The use of digital appointment scheduling and telemedicine has increased participation in diagnostic services.

Southeast Asian nations like Thailand, Indonesia, Vietnam, and Malaysia, are steadily improving their markets. Their government’s focus is on laboratory and disease monitoring programs. They are also looking into improving the early detection of infectious diseases and screening programs for diabetes and heart diseases. Diagnostic devices that are portable are well suited for this region’s varying geography and the healthcare disparities present.

With a focus on innovation, Singapore and South Korea invest in precision medicine and diagnostics. They also utilize advanced molecular testing, diagnostic automation and integrated health (data) diagnostics. Their collaborative health research and biotechnology ecosystems improve the region’s adoption of diagnostic technologies.

Middle East and Africa

By 2026, the Middle East and Africa region’s (MEA) in vitro diagnostics (IVD) will be influenced by healthcare improvements in the region due to the recent construction of medical facilities, greater awareness and understanding of the necessity of diagnostics, and increasing government initiatives to develop systems for proactive preventative healthcare. The MEA region contains both ends of the spectrum in terms of maturity level; technologically advanced healthcare markets in the Middle East and in Africa, incipient developing (diagnostic) systems in various (developing) countries. The region’s healthcare systems, as an ecosystem, are completing their cycle, and as the systems propel advancements, more countries will begin to realize the importance of sophisticated diagnostic systems.

The ecosystem’s advanced cycle will be stimulated by the global understanding of the necessity for early and accurate diagnostics and the regional understanding of the necessity for early and cost-effective healthcare. This understanding will enhance the efforts of clinical laboratories and hospitals to establish and strengthen their diagnostic systems which will, in turn, help establish a sophisticated healthcare ecosystem.

An overview of the diagnostic device market illustrates the advanced capabilities of the Middle East healthcare system. As a result of ongoing healthcare modernization efforts, the Middle East, and more specifically countries like Saudi Arabia and the United Arab Emirates, experience less dependency on patients traveling abroad for medical assistance.

Automation in diagnostics and integrated laboratory systems has been widely adopted by hospitals, and this is increasingly becoming the case for hospitals dealing with large numbers of patients, particularly those with several chronic conditions. High-quality clinical diagnostic systems are needed to address the healthcare demands created by the increasing number of private healthcare systems and the dominance of medical tourism. High-quality diagnostics are particularly in demand for health assessments, oncology screening, and infectious disease monitoring.

Israel produces significant regional innovation through biotechnology and advanced diagnostics. Innovative methodologies pave the wave for new partnerships to produce new technologies for precision diagnostics and personalized medicine. New methods of digital integration of clinical workflow laboratories and patient information systems will be useful for diagnostic turnaround time improvement and clinical decision-making.

In the North African region of Sub Saharan Africa (SSA), Egypt and Morocco are developing new diagnostic technologies for hospital construction and new diagnostic technologies for hospital construction and new public health screening programs. New infections are emerging, and new methods of urban health services and laboratory training are further developed to make the new diagnostic methods available.

In the region, Sub Saharan Africa has the most undervalued potential for the development of the IVD industry. New laboratory networks are developing new IVD testing methodologies in South Africa, Kenya, and Nigeria. New portable and affordable testing methodologies are developing new IVD testing methodologies in South Africa, Kenya, and Nigeria. Testing methodologies for new vaccines are being developed in many countries to address the new rural road networks.

Frequently Asked Questions with Answers

What is the In Vitro Diagnostics market size and growth forecast?

In Vitro Diagnostics Market is projected to reach a value of USD 13.4 Billion in 2025 and is anticipated to grow to approximately USD 178.3 billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 4.3% during the forecast period from 2026 to 2034.

Who are the key players in the In Vitro Diagnostics market?

The In Vitro Diagnostics Market Includes Major Companies Abbott Laboratories, Agilent, Becton Dickinson, bioMérieux, Bio-Rad, Danaher Corporation, DiaSorin, Exact Sciences, Fujifilm, Gold Standard Diagnostics, Grifols, Hologic, Illumina, LabCorp, Qiagen, Quest Diagnostics, QuidelOrtho, Roche, Siemens Healthineers, Sysmex, Thermo Fisher Scientific, Others.

What are the current and future trends for In Vitro Diagnostics market?

Due to the increasing need for the detection of chronic diseases and integration with digital healthcare, the In Vitro Diagnostics market is moving towards artificial intelligence oriented diagnostics, molecular and precision testing, automated and precision testing, and more decentralized diagnostics and patient-centric at home testing solutions.

Which regions dominate the In Vitro Diagnostics market?

The IVD market is led by North America, with Europe in second place and Asia-Pacific as the market with the highest growth rate.

Key insights provided by the report that could help you take critical strategic decisions?

- Regional reports analyse product/service consumption and market factors in each region.

- Reports highlight possibilities and dangers for suppliers in the In Vitro Diagnostics Market business globally.

- The report identifies regions and sectors with the highest growth potential.

- It provides a competitive market ranking of major companies, as well as information on new product launches, partnerships, business expansions, and acquisitions.

- The report includes a comprehensive corporate profile with company overviews, insights, product benchmarks, and SWOT analysis for key market participants.

Customization: We can provide following things

1) On request more company profiles (competitors)

2) Data about particular country or region

3) We will incorporate the same with no additional cost (Post conducting feasibility).

Any Requirement Contact us: https://www.forinsightsconsultancy.com/contact-us/

Table of Contents

For TOC Contact us: https://forinsightsconsultancy.com/contact-us/