Herbicides Market Growth Analysis Research Report By Type: Synthetic Herbicides, Bio-based / Organic Herbicides; Form: Liquid Herbicides, Granular Herbicides, Powder Herbicides; Mode of Action: Selective Herbicides, Non-Selective Herbicides;- and Global Forecast to 2034

Mar-2026 Formats | PDF | Category: Agriculture | Delivery: 24 to 72 Hours

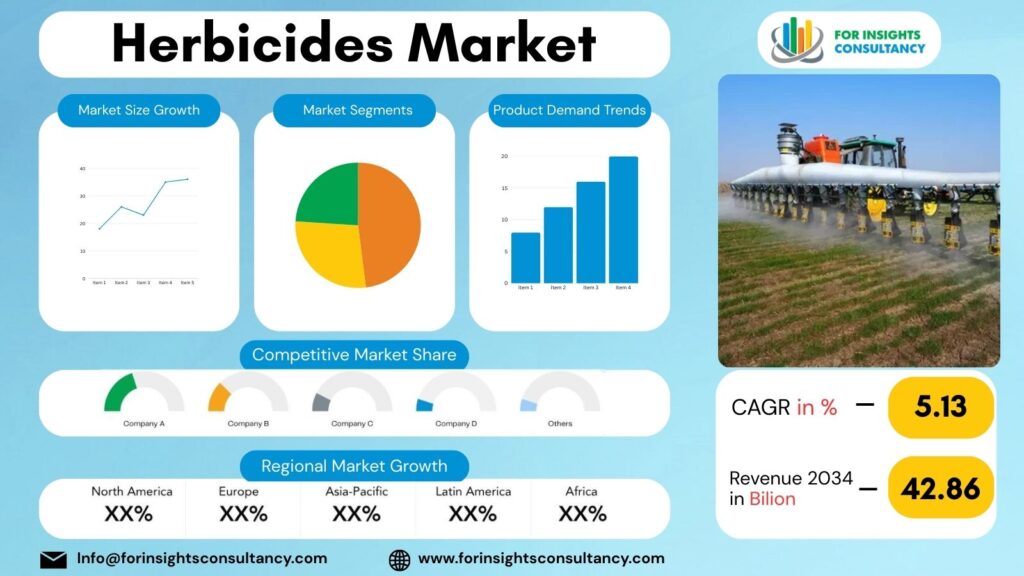

Herbicides Market Size & Forecast: Industry to grow from USD 42.86 Billion (2025) to USD 67.34 Billion (2034) with 5.13% CAGR. See growth drivers and demand trends.

Overview of the Herbicides Market and Expected Growth (2026)

The Herbicides Market is predicted to grow steadily by 2026 along with developments in global agriculture focused on better crop yields and weed management systems. Herbicides are chemical or biobased products designed to control or kill unwanted weeds that compete with crops for nutrients, sunlight, and water. In an Integrated Crop Management (ICM) framework, herbicides are used to reduce the degree of weeding by hand, and give the opportunity to stabilize yields. Widespread adoption of herbicides is an answer to the increasing food demands for the limited available arable land globally. This is true for developed farming economies, as well as emerging economies.

Market growth in 2026 will also be influenced by innovations in crop protection products and herbicides that reduce the impact on the environment, as well as increases the efficiency of applications. There is a focus on precision farming systems, and herbicides that are effective in combination with genetically modified crops (GMC) of lower toxicity. There is a high demand for the use of herbicides in extensive farming areas with mechanized agriculture, as well as for weed control on large areas. On the contrary, the need for sustainable agricultural systems and effective weed management is the reason for the development of biobased herbicides and other integrated approaches.

The enhanced cultivation of high-value crops like fruits, vegetables, and oilseeds, where weed management directly influences the quality and profitability of the crops, is another key driver of this growth. Along with the advent of new agricultural chemicals, the adoption of herbicides is also rising in developing agricultural markets where farmers have access to contemporary crop protection inputs, agricultural extension services, and better communication and distribution systems. As the changing climate affects the distribution of weeds and the cycle of crops, farmers will increasingly depend on effective herbicides to achieve stable yields, reiterating the importance of herbicides in the management of crops to be protected in 2026.

Market Dynamics 2026

Growth Drivers

Growing Adoption of Precision Farming Agri-tech tools like satellite imaging and GPS-guided sprayers engages targeted herbicide use. Precision farming tech enables herbicide use to be more efficient and both economically and environmentally rational consider weed management. The integration of digital tech into farming practices is a priority for the Food and Agriculture Organization when funding research.

Government Backing of Farming Practice Enhancement Many governments are developing policies and farming research programs to address the dual challenges of increasing crop yield and ensuring a reliable supply of food. Their focus is often on facilitating the use new weed management methods, including herbicides. For example, the US Department of Agriculture funds research into better managing weeds.

Restraints

Stringent Regulations Around the Approval of New Chemicals – Herbicides are thoroughly evaluated for potential toxicity and impact on the environment before they can be approved for commercial use. As part of the evaluation process, manufacturers must submit extensive scientific documentation to The European Food Safety Authority and other organizations, resulting in lengthy and expensive product approval processes.

Increased Interest in Organic and Chemical-Free Farming – As organic farming continues to grow in popularity, more and more farmers are being compelled to pursue non-chemical methods of weed management, such as crop rotation, mulching, and mechanical control. Farming systems that promote the use of non synthetic herbicides is supported by the International Federation of Organic Agriculture Movements.

Opportunities

Advancement of Bio-Based Herbicides – Growing concern for the environment offers potential for the development of bio-based herbicides made from plant or natural sources. Agricultural scientists and advocates for sustainable agriculture, including the Food and Agriculture Organization, promote the development of sustainable weed management alternatives that protect the environment.

Integration of Precision Agriculture Techniques – The use of GPS-based technology, drones, and intelligent spraying devices is allowing farmers to spray herbicides with greater precision for reduced chemical application. This improves weed control and increases the need for and precision farming suitable herbicides.

Challenges

Expanding populations of herbicide-resistant weeds – The rapid emergence of new weed species resistant to popular active ingredients is one of the leading challenges to the herbicide market’s profitability. The remaining patened herbicides have declining efficacy due to the predictable weed-control strategies fostered by the herbicide’s mode of action. Fleeting remaining herbicides placed growing economic burdens on farmers as herbicides became ineffective. This growing economic burden and the increasing number of resistant weed populations have been documented in studies funded by the Weed Science Society of America and the world over.

Increased environmental and safety regulations – The environmental and safety concerns of using agrochemicals have led governments to limit the use of applied science in pest control. For example, the European Food Safety Authority, one of the risk assessors for the use of pesticides, evaluates the environmental and human health risks posed by pesticides. The need to adhere to these requirements may lengthen the time it takes to introduce new agrochemicals and/or increase the number of pesticides for sale.

Top Companies Covered In This Report

(Major global and regional players shaping the industry)

- Bayer AG

- Syngenta Group

- BASF SE

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- ADAMA Agricultural Solutions

- Nufarm Limited

- Sumitomo Chemical Co., Ltd.

Herbicides Industry Company News 2025 and 2026

Bayer AG

In 2026, the company continued restructuring its crop science division to improve profitability and manage litigation linked to its herbicide portfolio such as Roundup. Bayer is also developing next-generation herbicide technologies such as icafolin-methyl to address herbicide-resistant weeds and support sustainable farming practices.

Syngenta Group

In 2026, the company announced it will stop global production of the paraquat herbicide by June 2026, citing strong competition from generic products and strategic portfolio shifts.

In 2025, Syngenta also reported progress on a new herbicide chemistry subclass aimed at controlling grass weeds that have developed resistance to existing herbicides.

BASF SE

In 2026, BASF partnered with Corteva Agriscience to launch the Clearfield mustard production system in India, a herbicide-tolerant crop solution designed to improve weed control and crop yield.

BASF also collaborated with ADAMA Agricultural Solutions on crop-protection technology development to expand advanced agrochemical solutions for farmers.

Corteva Agriscience

In 2025, the company expanded its crop protection portfolio by launching new herbicides and insecticides focused on improving resistance management and crop productivity in major farming regions. In 2026, Corteva collaborated with BASF to introduce herbicide-tolerant crop systems targeting better weed control in mustard farming.

Detailed Segmentation and Classification of the report (Market Size and Forecast – 2034, Y-o-Y growth rate, and CAGR):

Type:

- Synthetic Herbicides

- Bio-based / Organic Herbicides

Form:

- Liquid Herbicides

- Granular Herbicides

- Powder Herbicides

Mode of Action:

- Selective Herbicides

- Non-Selective Herbicides

Application:

- Foliar Spray

- Soil Treatment

- Seed Treatment

Crop Type:

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Turf & Ornamental Crops

End User:

- Agriculture

- Forestry

- Industrial Vegetation Management

- Residential & Commercial Lawn Care

Regional Deep-dive Analysis:

The report provides in-depth qualitative and quantitative data on the Herbicides Market for all of the regions and countries listed below:

North America

North America has a unique herbicides market and by 2026 will likely see even further innovation. With large-scale commercial farming and precise farming, North America has also increased their technological advancements in weed management.

United States:

In North America, the largest percentage of herbicides usage comes from the United States because of the large farming of corn and soybeans. Certain species of weeds have become resistant to certain herbicides, forcing farmers to adopt integrated weed management and some other advanced herbicide techniques to combat these weeds.

Canada:

Demand for herbicides in Canada comes primarily from the farming of cereals and oilseeds, particularly wheat and canola. Farmers have increased their use of crop systems that are resistant to herbicides, and have increased their use of herbicides that have different mechanisms of action in order to sustain high yields and not run afoul of environmental laws.

Mexico:

Mexico has been increasing herbicides use due to the improvement of farming techniques and also the increased farming of maize, fruits, and vegetables. The government encourages more sustainable farming and crop protection, and as a result, the use of more efficient weed control mechanisms has been encouraged.

Europe

Significant agricultural productivity coupled with stringent environmental regulations will influence the European herbicides market for 2026. In the region, farmers are increasingly using integrated weed management (IWM) practices, combining chemical herbicides with mechanical and biological methods.

Western Europe:

Western Europe commands the largest market share from the regional herbicide market, with France, Germany and the United Kingdom exhibiting significant herbicide use owing to their intensive agricultural practices. Farmers make use of innovative herbicide technologies and precision spraying systems to control weeds in extensive areas of cereal and grain cultivation.

Southern Europe:

Southern Europe experiences steady demand for herbicides owing to the region’s production of commercially valuable herbaceous plants, including grapes, olives, vegetables and citrus fruits. With the advent of warmer climatic conditions, effective weed management systems are significant for the conservation of soil moisture and the enhancement of crop yield.

Eastern Europe:

As agricultural activities in Eastern Europe become more modernized, a more rapid increase in herbicides is expected. The expansion of commercial farming in Poland, Hungary and Romania stimulates the use of crop protection products in the cultivation of cereals and oilseeds.

Northern Europe:

Northern European countries put a focus on the sustainable aspects of farming and agriculture. For example, the herbicides used in Sweden, Denmark and Finland are carefully regulated and used in conjunction with environmental impact considerate integrated weed management strategies.

Asia-Pacific

The Asia-Pacific herbicides market 2026 features developing agricultural output, growing demand for food, and the market’s steady adoption of effective weed control technologies. In the Asia-Pacific markets, farmers rely more on integrated weed management and herbicides to protect the yields of rice, wheat, and corn.

China:

The Asia-Pacific herbicides market counts China as a dominating competitor due to one of the largest agricultural sectors, as well as one of the largest agrochemical industries. In China, herbicides are commonplace for weed management in rice, corn, and wheat, as well as for the maintenance of all crop productivity.

India:

India’s market for herbicides grows as farmers move from manual to chemical weed control. Demand for herbicides is high in irrigation and mechanized farming, as well as in the primary crops classified as rice, wheat, cotton, and sugarcane.

Japan:

Japan’s agricultural market is sophisticated and herbicide application is uniform and extensive. Safer herbicide use is the outcome of managed precision agriculture and regulated herbicide environments.

Southeast Asia:

The Philippines, Vietnam, Indonesia, and Thailand are Southeast Asian countries with increased herbicide demand due to extensive rice cultivation and large scale plantations. The adoption of herbicides is driven by the desire to reduce labor and improve the efficiency of farming.

Australia & New Zealand:

This subregion depends on the use of herbicides to assist in the large scale farming of grains and oilseeds. Farmers focus on the management of herbicide resistance and sustainable practices of weed control to ensure long-term productivity of the agriculture.

Middle East and Africa

The Middle East & Africa region’s herbicides market is estimated to increase to USD $260 million by 2023, and 2023 to USD $320 million by 2023. This increase can be attributed to farmers’ need to improve their productivity of their crops. High weed pressure is a universal challenge to agriculture productivity. This is especially true for the Middle East & Africa region as extreme climate conditions hamper crop production.

Middle East:

In Saudi Arabia, Israel, and the United Arab Emirates, herbicides are used for irrigation and greenhouse farming. In water-scarce agriculture, herbicides are used for growing cereals, vegetables, and fruits.

North Africa:

In North African countries such as Egypt, Morocco, and Tunisia, agriculture is organized, and herbicides are used in irrigation and rain-fed wheat, barley, and vegetables.

Sub-Saharan Africa:

Sub-Saharan Africa is in great need of herbicides. They are reducing manually done weed control in thousands of farms. They are reducing costs and increasing the productivity of crops grown. However, the adoption of herbicides is highly uneven.

Southern Africa:

Southern Africa, especially South Africa, has one of the most advanced agricultural markets in the region. Commercial farms use herbicides to control weeds in maize, wheat, and soybean crops, sustained large-scale farm productivity.

Frequently Asked Questions with Answers

What is the Herbicides market size and growth forecast?

Herbicides Market is probable to reach a value of USD 42.86 Billion in 2025 and is anticipated to grow to almost USD 67.34 Billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 5.13% during the forecast period from 2026 to 2034.

Who are the key players in the Herbicides market?

The Herbicides Market Includes Major Companies Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, FMC Corporation, UPL Limited, ADAMA Agricultural Solutions, Nufarm Limited, Sumitomo Chemical Co., Ltd., Others.

What are the current and future trends for Herbicides market?

There is growing adoption of bio-based herbicides, precision agriculture technologies, herbicide-tolerant crops, and environmentally friendly formulations for better weed management, increased control of the environmental impact, and decreased use of chemicals.

Which regions dominate the Herbicides market?

North America and Asia-Pacific dominate the global herbicides market due to large-scale crop cultivation, advanced farming practices, and strong demand for effective weed management solutions.

Key insights provided by the report that could help you take critical strategic decisions?

- Regional reports analyse product/service consumption and market factors in each region.

- Reports highlight possibilities and dangers for suppliers in the Herbicides Market business globally.

- The report identifies regions and sectors with the highest growth potential.

- It provides a competitive market ranking of major companies, as well as information on new product launches, partnerships, business expansions, and acquisitions.

- The report includes a comprehensive corporate profile with company overviews, insights, product benchmarks, and SWOT analysis for key market participants.

Customization: We can provide following things

1) On request more company profiles (competitors)

2) Data about particular country or region

3) We will incorporate the same with no additional cost (Post conducting feasibility).

Any Requirement Contact us: https://www.forinsightsconsultancy.com/contact-us/

Herbicides Market Top queries

how are Herbicides made

Herbicides consist mainly of renewable biomass such as starch from plants (like corn and sugarcane) and from cellulosic and soy protein sources, as well as from biomass-based microbial polyesters (PHA). Examples are Polylactic Acid (PLA) resulting from the fermentation of plant starch, and Polyhydroxyalkanoates (PHAs) from bacterial sources. These substances will be broken down to water, CO2 or methane.

what are Herbicides

Herbicides are made to decompose as a result of microorganisms (bacteria and/or fungi) to water, carbon dioxide and biomass, and only in certain situations. These types of plastics are made from renewable resources such as starch and cellulose, and are used in packaging, farming, and medical uses.

are plastics biodegradable

Standard types of plastics do not decompose naturally. Instead, they break into tiny pieces known as microplastics which can last for hundreds of years. Some commercially available products are described as “Herbicides”. However, these products do not decompose in a natural environment. They are only considered biodegradable if they decompose in a designated industrial composting facility.

Table of Contents

For TOC Contact us: https://forinsightsconsultancy.com/contact-us/