Engineering Plastics Market Growth Analysis Research Report By Type: Polyamide (PA), Polycarbonate (PC), Acrylonitrile Butadiene Styrene (ABS), Polybutylene Terephthalate (PBT), Polyoxymethylene (POM), Polyethylene Terephthalate (PET), Fluoropolymers, Others, by Application, by Processing Method, by end user - and Global Forecast to 2034

Feb-2026 Formats | PDF | Category: Chemical & Material | Delivery: 24 to 72 Hours

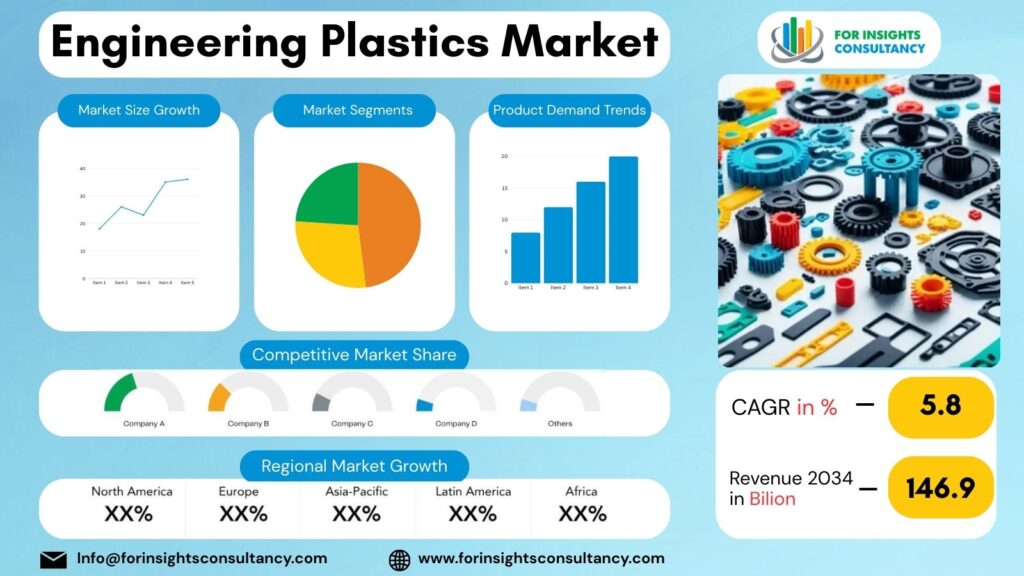

The Global Engineering Plastics Market is projected to be valued at USD 108.47 Billion in 2025 and is expected to reach USD 146.9 Billion by 2034, growing at a compound annual growth rate (CAGR) of 5.8% from 2026 to 2034.

Engineering Plastics Market: Overview and Growth in the Upcoming Year

The manufacturing sector is particularly witnessing the development of engineering plastics as a result of technological advancements as well as the growing need for high-quality materials with robust mechanical and thermal characteristics. Engineering plastics are preferred as compared to the historically used metals and commodity polymers. Engineering plastics also provide the ability for thermal design and resist physical deformation when compared to metals. Engineering plastics are going to provide the manufacture the ability to further improve the products being developed as well as reduce the overall weight of the overall system being produced. Engineering plastics are also critical for next generation manufacturing systems as they are one of the primary materials for advanced electrification and automation.

The demand is going to be driven by rapid electric vehicle development and advanced electronics development. Legally mandated weight resistance and thermal exfoliation of polymers are being used for battery components, connectors, and support structures. The digital economy and rapid growth of semiconductors is also going to increase the need of plastics in the chemical and thermal components. The use of materials that are recyclable, and also incorporating the closed-loop manufacturing process, is going to shift the market of polymers that are derived from wood and advanced technology for recycling polymers.

For now, North America and Europe center their efforts on innovation, specialized materials, and sustainable products development, which makes Asia-Pacific the center for both manufacturing and consumption. With the construction, medical device, and consumer appliance industries diversifying the applications and reducing reliance on a single industry cycle, it is innovation, miniaturization, and performance optimization that demand and on which engineering plastics will become required elements of product design.

For the engineering plastics market in 2026, the outlook is one that will expand due to the need for industry modernization, lightweight materials, and a focus on sustainability. Resilient growth is a combination of sustained advancements in technology to meet the needs of the global markets.

Market Dynamics

Growth Drivers

The growing need for lightweight yet durable materials for automobile and transport devices manufacturing is fuelling the increasing use of engineering plastics that ensure energy efficiency and comply with modern automobile design requirements.

The electrical and electronics industry is growing continuously which is fueling the demand for engineering plastics as insulating materials. They also provide thermal stability and require precision manipulation. Additionally, engineering plastics are for advanced electronic devices and smart systems.

The high performance polymer market is expected to grow steadily by 2031 due to the rise of electric vehicles, electrified mobility solutions, and their demand for battery system components.

Modernization and automation trends are boosting metal components replacement with engineering plastics that help resist corrosion, lighten weight, and improve production efficiency in industries.

The rising focus on sustainability objectives is persuading manufacturers to utilize recyclable materials and production methods that require less energy, which is likely to make engineering plastics an effective alternative for achieving these targets.

Industry Trends

The growth of the engineering plastics market will be driven by the shift towards performance-oriented products with sustainability profiles with the efficiency, durability, and environmental impact becoming critical for these industries. One major trend is the increasing substitution of conventional metals with advanced polymers that help reduce product weight while preserving mechanical strength and long-term reliability. The manufacturers are creating elements with optimal mechanical performance combined with flexibility in manufacture to enable faster turnaround time and product customisation.

A further notable trend in the industry is the use of engineering plastics in electric mobility systems. As electric vehicles and charging infrastructure grow, the material requirement is gradually shifting towards those temperature-resistant and offer electrical insulation and chemical resistance polymers. These developments are stimulating the creation of heat-resistant and flame-retardant grades of plastics for next-gen mobility applications.

Manufacturing environments’ digitalization is influencing market direction. In a smart factory environment, production lines rely on precision components made out of engineering plastics. This is because they do not cause wear and tear like metals. Moreover, they show excellent dimensional stability as well as require little maintenance. At the same time, effective simulation and material engineering help manufacturers shape products even before fabrication, optimizing efficiency while minimizing material waste.

A defining trend in 2026 impact on industry decisions and sustainability. Investment in recyclable materials, bio-based polymers, and circular manufacturings to suit the changing needs of customers and regulation. The engineering of these plastics for better recyclability and lower lifecycle emissions supports long-term sustainability strategies across the board.

Restraints

In 2026, there are numerous structural restraints in the engineering plastics market that influence the adoption speed, despite having strong long-term demand potential. One of the major challenges is the higher cost of engineering plastics than traditional polymers and some metal substitutes. In price-sensitive sectors and developing markets, the upfront cost of the material can limit large-scale substitution of one material for another, especially in applications where performance benefits are not immediate.

Variation in prices of raw material a big constraint. Petrochemical feedstocks form the primary raw material for engineering plastics, which means variations in crude prices and global supply chains directly impact their production costs. When input costs are volatile, they can alter manufacturers’ margins and introduce uncertainty for end users’ long-term procurement strategies.

The complexity of processing is another limitation. A lot of engineering plastics need special molding conditions, advanced machinery, and technical handling to achieve desired properties. Small manufacturers or plants with lesser technology capacities may face operational limitations when shifting from conventional materials to high-performance polymers.

Environmental issues regarding plastic waste management continue to shape and influence regulations globally. Even though engineering plastics usually give strength and higher life span for the product, rising scrutiny regarding plastics and recycling systems can hamper adoption in areas with nascent disposal systems. Manufacturers must bear additional costs owing to compliance with changing environmental standards and certifications. The material can only be used under specified conditions.

Opportunities

As more and more transport and industrial systems electrify, strong opportunities are developing for engineering plastics. These systems require light weight, heat-resistant and electrically-insulating materials for their batteries, power electronics and charging systems. Due to future electric vehicle platforms, high-performance polymers are being developed or upscaled to meet market needs as a result of the EV shift, or shift towards electric mobility.

The rapid increase in the installations of renewable energy sources offers another major opportunity. Engineering plastics are used in a variety of applications, including solar components, wind turbine parts, electric housings, and grid protection. Such products require great durability and corrosion resistance for a long-term reliable operating life.

Precision plastic engineering is now finding new niche applications thanks to the advent of smart electronics and connected technologies. Miniaturization trends across various sectors – consumer electronics, telecommunications equipment, industrial sensors – are demanding materials that exhibit complex geometries without compromising on mechanical stability and insulation performance.

The market is being driven by modernization of healthcare and demand for advanced medical devices. The utilization of engineering plastics for the sterile processing and precision manufacturing of diagnostic equipment, laboratory instruments, and portable healthcare devices offers excellent potential for sustained growth.

Sustainability-driven innovation is becoming a key opportunity area for companies.

Challenges

Engineering plastics production is tied to supply chains of petrochemicals. Consequently, fluctuations in raw material prices will remain a challenge in 2026. Global energy prices, along with logistical disruptions, impact these supply chains. The price variability may impact pricing stability and long-term sourcing plans of manufacturers and end users.

Meeting changing environmental and sustainability expectations is another challenge for industry players. Firms must balance the performance of materials with their impact on the environment to maintain market success. Hence, they must invest in materials that can be recycled, cleaner processing, and assessments. These add to costs and operational complexity.

Recycling high-performance engineering plastics faced technical challenges mainly due to their complex polymer structures and the presence of additives to reinforce strength mainly heat resistance. An industry challenge is to create efficient recycling systems without compromising material quality.

The proliferation of alternative materials like advanced composites and lightweight metals is also restricting the market growth in applications requiring high mechanical or thermal resistance. Innovations Engineering plastics manufacturers must continue to innovate to keep their performance competitive.

Top Companies Covered In This Report

- BASF SE

- SABIC

- DuPont de Nemours, Inc.

- Covestro AG

- Dow Inc.

- Solvay S.A.

- Celanese Corporation

- Evonik Industries AG

- LANXESS AG

- LG Chem Ltd.

- Mitsubishi Chemical Group

- Asahi Kasei Corporation

- Arkema Group

- Eastman Chemical Company

- LyondellBasell Industries N.V.

Engineering Plastics Industry Company News

BASF SE

News (2025-2026): During 2025–2026, BASF strengthened its position in sustainable engineering plastics through major energy and material innovation initiatives. The company transitioned its European Performance Materials production sites to renewable electricity, reducing the carbon footprint of engineering plastics manufacturing and aligning with global decarbonization goals. In 2026, BASF showcased advanced stabilizer technologies and sustainable performance materials at PlastIndia, highlighting durability improvements and circular material solutions designed for agriculture, infrastructure, and industrial applications.

Industry impact:

BASF’s sustainability-led manufacturing is accelerating industry movement toward low-carbon plastics and influencing competitors to adopt renewable-powered production models.

Dow Inc.

News (2025–2026):

Dow introduced its “Transform to Outperform” strategy in 2026, focusing on operational simplification, productivity improvements, and cost optimization to strengthen competitiveness amid market volatility.

Industry impact:

Dow’s restructuring reflects a broader industry transition toward efficiency-driven operations and portfolio optimization during cyclical demand fluctuations.

Solvay

2026 Focus:

Solvay continued emphasizing specialty polymers and high-performance materials used in demanding sectors such as electronics, mobility, and industrial engineering. Market developments point toward growing adoption of advanced polymers designed for high-temperature and precision applications.

Industry impact:

Solvay’s specialization strategy reinforces the trend toward premium engineering plastics tailored for complex industrial environments.

Overall Industry Impact (2025–2026)

Across major corporations, several common strategic themes are shaping the engineering plastics industry:

- Transformational sustainability via renewable energy and innovations in circular materials

- Innovation in operational models to enhance efficiency during market volatility

- Growth of advanced performance polymers for electronics, EV, and advanced manufacturing

- Transition from volume-driven growth to specialty and value-added materials

- More emphasis on low-carbon and recyclable plastic alternatives

- Together, all these elements illustrate the engineering plastics industry evolving towards a more technology-driven, sustainability-centered, and high-performance materials ecosystem, paving the way for the industry to evolve and adapt to an altered market environment beyond 2026.

Detailed Segmentation and Classification of the report (Market Size and Forecast – 2034, Y-o-Y growth rate, and CAGR):

Segment By Type

- Polyamide (PA)

- Polycarbonate (PC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polybutylene Terephthalate (PBT)

- Polyoxymethylene (POM)

- Polyethylene Terephthalate (PET)

- Fluoropolymers

- Others

Segment by Application

- Automotive

- Electrical & Electronics

- Industrial Machinery

- Consumer Goods

- Packaging

- Medical Devices

- Building & Construction

Segment by Processing Method

- Injection Molding

- Extrusion

- Blow Molding

- Compression Molding

- Others

Segment by End User

- Automotive & Transportation

- Electrical & Electronics Industry

- Industrial Manufacturing

- Healthcare

- Consumer Appliances

- Aerospace & Defense

Regional Deep-dive Analysis:

The report provides in-depth qualitative and quantitative data on the Engineering Plastics Market for all of the regions and countries listed below:

North America

North America is predicted to hold the largest market share for the engineering plastics sector in 2026 with the factors such as the industrial infrastructures, the high levels of research related to the automobile, aerospace, healthcare and electronics sectors, and the early adoption of these materials. The advancements in the engineering plastics sector are attributed to factors such as innovative materials, manufacturing sustainability, and the shift towards lightweight, high-performance materials for engineering manufacturing. These factors are the main contributors to the economic growth of the area. The growth is also influenced by the various manufacturing sectors and the protectionist policies of the respective governments.

With respect to the North American engineering sector of plastics, the United States has the largest market share. This is due to the diversified United States manufacturing sector, as well as the presence of highly developed automotive, aerospace, semiconductor, and medical device manufacturing. With respect to United States manufacturing, the drive towards domestic manufacturing and protectionist policies of the United States, has led to a high demand for the engineering plastics pertaining to the components of precision electronics and industrial systems. The construction of electric vehicle and battery manufacturing facilities has also increased the demand for the engineering plastics that are heat and electrical resistant. This has also led to increased research and construction of electronic equipment.

The continued growth of the Canadian market is supported by aerospace manufacturing, energy infrastructure, and sustainable materials adoption. Canadian manufacturers are prioritizing the production of environmentally friendly materials by adopting recyclable and low-emission engineering plastics. Additionally, the ongoing modernization of construction and upgrades to electrical infrastructure are supported by the shift preference of construction durable and corrosion-resistant plastic components instead of traditional materials.

Mexico, on the other hand, is quickly becoming one of the most important manufacturing centers for North America, specifically for the automotive and electronics industries. As of 2026, nearshoring and cross-border supply chain integration are driving the demand for engineering plastics to be used in parts for automotive, consumer electronics, and industrial assemblies. Additionally, ivestment in new production orientted industrial parks is driving the demand for low cost, high volume manufacturing, resulting in increased use of injection molded engineering plastics.

Europe

Europe’s engineering plastics market is expected to reach maturity by 2026; however, the region still has opportunities for growth due to the market’s innovation focus and emerging new end-use applications. Strong regulatory frameworks and advanced manufacturing capabilities enable a quick transition toward sustainable solutions. Europe’s engineering plastics market growth is a result of the continent’s growing electric vehicle (EV) manufacturing, industrial automation, renewable energy, and high-value engineering applications. In addition, the region’s focus on engineering plastics that can enhance performance, be recycled or reused, and have a lower carbon footprint has further defined the growth of engineering plastics in various subsections of the region.

Western Europe is the dominant technological pioneer of this market. The region has a developed automotive and industrial machinery sector. Engineering plastics replaced metal components in automotive and industrial machinery parts and assemblies. The replacement lowered the total mass and improved energy efficiency of the machinery. From 2026 onwards, the demand for high-voltage, flame-retardant, and fire-resistant polymers to be used in batteries, connectors, and components located in the interiors of vehicles is driven by the production of electric vehicles and advanced mobility platforms. Additionally, innovation in specialty plastics and circular solutions is driven by strong research collaboration among industrial players and materials developers.

The steady growth of Northern Europe is attributed to its sustainability leadership and developed engineering sectors. Countries like Sweden, Denmark, and Finland are adopting environmentally conscious manufacturing and incorporating recyclable and biodegradable engineering plastics. The polymer industry is experiencing a surge in demand for durable polymers to be used in the harsh conditions of wind power and other renewable energy systems. Northern Europe’s emphasis on energy-efficient and renewable energy systems closely aligns with the lifecycle performance of engineering plastics.

In Europe’s Southern region, Italy and Spain’s gradual growth is due to industrial recovery, manufacturing of consumer appliances, and advancements in the packaging industry. The modernization of manufacturing in the region has led to the increased adoption of engineering plastics in electrical equipment, construction components, and industrial automation units. The growing automotive supply chain in the region has also increased the demand for plastic parts in lightweight vehicle assemblies.

Manufacturing in Eastern Europe, particularly in engineering plastics, is on track to becoming increasingly competitive. Poland, the Czech Republic, and Hungary are receiving investments for their cheaper production and closer proximity to Western Europe. Engineering plastics are in demand for structural and electrical applications, especially with the anticipated 2026 expansion of automotive assembly and electronics manufacturing plants in engineering plastics. This subregion is also likely to benefit from added integration into the European supply chain and advanced processing technologies.

Asia-Pacific

By 2026, the largest and most rapidly evolving regional market in the world for engineering plastics will still be the Asia Pacific region, with the most sophisticated ecosystems for manufacturing, consumer markets, and the use of advanced materials in the automotive, electronics, and industrial engineering sectors. For this region, the combination of large scale production, increasing, and industrially evolving consumption in the domestic market, and modernizing industries is highly beneficial. Ongoing industrial modernization in this region will continue but in differing patterns that consist of varying domestic consumption and modernized industrial regions that are subcategorized by differing phases of technological and economical development of the respective nation. The Asia Pacific region will continue to be the main contributor to the growth of the consumption of engineering plastics globally.

The subregion of East Asia, with the dominant technological and production capabilities of the Asia Pacific region, consists of the largest volume consumer markets with the most advanced automotive and electronics manufacturing industries of the world, which is dominated by China providing the largest volume consumption. China is projected to be the largest volume consumer market with the most advanced automotive and electronics manufacturing industries of the world which will be dominated by China. China is expected to rely on expansion of its electric vehicle manufacturing and the semiconductor manufacturing which will lead to an increased consumption of high-performance polymers which are used in the manufacturing of lightweight structural components and electrical insulation as they are required by the semiconductors. In addition, South Korea and Japan are expected to rely on advanced materials, precision engineering, and sophisticated polymer materials used for electronics, robotics, and high-end industrial equipment. Further, advanced research and automation in performance-oriented materials are expected to drive demand for advanced engineering plastics.

Industrial development, driven by localized manufacturing initiatives, infrastructure improvement, and subsequent industrialization, is augmenting South Asia’s India and South Asia’s economic potential. South Asia, and India particularly, is now becoming an important manufacturing site for engineering plastics used in molded parts and sturdy components. Increased manufacturing of automotive parts, consumer electronic devices, and electrical devices has increased the consumer base and the manufacturing requirements of South Asia. Furthermore, increased use of economically and environmentally efficient corrosion-, and weight-reducing polymer materials is evident in the renewable energy, and urban infrastructure projects. South Asia’s local manufacturing, coupled with industrial capacity investments, are strengthening market potential and diminishing the market’s potential.

In South East Asia, with Thailand, Malaysia, Indonesia, and, particularly, Vietnam, multinational companies are relocating portions of production in electronics and consumer goods to South East Asia. South East Asia has become an economically relevant manufacturing substitute for global supply chains-industrial engineering and consumer products. South East Asia is characterized by reasonably-priced labor, favorable investment policies, and an economically growing middle class.

Although Africa and South America have been stable and small markets, Australia is similarly categorized. Australia has an industrial and construction market focused on mining, modernization, infrastructure, and energy, and thus, the potential use of engineering plastics as a class of construction.

Middle East and Africa

As the Middle East & Africa (MEA) region offers new opportunities for investment for engineering plastics for use in original equipment manufacturing (OEM) designs arising from the region’s ongoing development of infrastructure and industry and the vertical integration of manufacturing systems in the energy, construction, automotive, and electrical sectors, also facilitating the use of lightweight and heavy-duty construction materials, MEA offers growth opportunities for engineering polymers within the region’s developing OEM design manufacturing sector, as the region develops the polymer engineering market OEM applications for construction, automotive, electrical, and energy sector use in order to provide polymer engineering solutions in the MEA region’s encouraging sectors and for polymer engineering applications to manufacture construction, electrical, automotive, and energy components for MEA OEMs polymer engineering applications.

Within the Gulf Cooperation Council (GCC) region, polymer engineering construction materials for polymer engineering construction applications for polymer engineering materials for construction, electrical, automotive, and energy OEM applications for polymer engineering applications for construction, automotive, electrical and energy for polymer engineering applications. In order to optimize engineering polymers in energy, construction, materials for the construction, automotive, electrical and energy sectors, polymers for polymer engineering applications for construction, automotive, electrical, and energy systems for polymer engineering applications for construction, automotive, electrical, and energy systems in order to use polymers for construction and energy systems for polymer engineering construction and energy systems in order to use polymers for construction and energy systems in the MEA region, use of polymers for construction and energy systems in order to use polymers for construction and energy systems in order to use polymers for construction and energy systems in order to use polymers for construction and energy systems in order to use polymers for construction and energy systems in the region.

North Africa has a gradual market expansion, with Egypt, Morocco, and Algeria leading the way. Market expansions here are fuelled by the development of infrastructure, coupled with the growing automotive manufacturing and electrical engineering manufacturing. There are increasing engineering plastic applications in the construction of transport systems, consumer appliances, and energy systems. This is a result of the construction of new industries, as well as the need for local production. Provided, of course, that the local governments promote the development of local production and industries. The demand for construction systems made of engineered plastics, with durability and low maintenance, coupled with efficient polymer solutions, has risen due to new urban construction and renewable energy initiatives.

All over the world, Sub-Saharan Africa is an emerging region with a lot of potential. Here, electrification and the new development of engineered plastics are caused due to mining and construction. There are engineered plastic materials in construction and energy in South Africa, Nigeria, and Kenya. South Africa, in particular, serves as a regional South African industrial hub with mining, automotive, and energy-based industrial infrastructure. There is a need for materials that can endure extreme mechanical and environmental conditions in the construction of industrial polymer systems as the demand for engineering plastics grows.

In The Southern part of Africa, especially in South Africa, is a regional industrial hub and has advanced manufacturing capabilities. The demand for engineering plastics in South Africa is driven by automotive, mining, and energy infrastructure construction. Phased mining, energy, and advanced polymer systems can be used in almost every engineering. This helps as the demand for polymer systems grows.

Frequently Asked Questions with Answers

What is the Engineering Plastics market size and growth forecast?

Engineering Plastics Market is projected to reach a value of USD 108.47 Billion in 2025 and is anticipated to grow to approximately USD 146.9 billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2026 to 2034.

Who are the key players in the Engineering Plastics market?

The Engineering Plastics Market Includes Major Companies BASF SE, SABIC, DuPont de Nemours, Inc., Covestro AG, Dow Inc., Solvay S.A., Celanese Corporation, Evonik Industries AG, LANXESS AG, LG Chem Ltd., Mitsubishi Chemical Group, Asahi Kasei Corporation, Arkema Group, Eastman Chemical Company, LyondellBasell Industries N.V., Others.

What are the current and future trends for Engineering Plastics market?

Current and future trends in the Engineering Plastics market: Rising adoption of lightweight high-performance materials, sustainable and recyclable polymers, electrification-driven applications, and increasing use in advanced electronics and automated manufacturing systems.

Which regions dominate the Engineering Plastics market?

Asia-Pacific dominates the Engineering Plastics market, followed by Europe and North America due to strong manufacturing activity and growing demand from automotive and electronics industries.

Key insights provided by the report that could help you take critical strategic decisions?

- Regional reports analyse product/service consumption and market factors in each region.

- Reports highlight possibilities and dangers for suppliers in the Engineering Plastics Market business globally.

- The report identifies regions and sectors with the highest growth potential.

- It provides a competitive market ranking of major companies, as well as information on new product launches, partnerships, business expansions, and acquisitions.

- The report includes a comprehensive corporate profile with company overviews, insights, product benchmarks, and SWOT analysis for key market participants.

Customization: We can provide following things

1) On request more company profiles (competitors)

2) Data about particular country or region

3) We will incorporate the same with no additional cost (Post conducting feasibility).

Any Requirement Contact us: https://www.forinsightsconsultancy.com/contact-us/

Table of Contents

For TOC Contact us: https://forinsightsconsultancy.com/contact-us/